The headline sounds like a prediction from five years ago, but it is happening right now. Self-driving trucks have completed a full round trip across the United States, hauling commercial freight from the west coast to the east coast and back again. This is not a demonstration run for investors or a closed track test. This is real cargo, real miles, and a real business model that changes the calculus for autonomous trucking.

For years the autonomous trucking conversation has centered on technology: when will the sensors be good enough, when will the software stop making mistakes, when will regulators say yes. Those questions are still important, but the real breakthrough that just landed is not about technology at all. It is about logistics. Specifically, it is about moving from a one way pilot to a round trip loop that makes the numbers work.

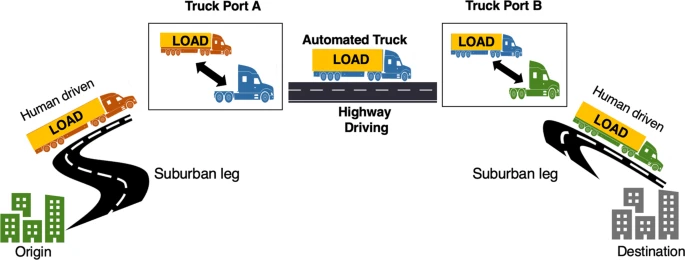

A major South Korean logistics provider has turned its autonomous trucking route across the United States into a full round trip operation. The trucks carry automotive parts from the west coast to the east coast and then pick up return freight for the journey back west. That second leg is everything. A truck that deadheads home empty costs the same in fuel and labor as a loaded truck but generates zero revenue. A round trip eliminates that waste, and in the thin margin world of freight, that difference is the line between a pilot project and a real business.

The ecosystem behind this achievement is worth examining because it shows how autonomous trucking is actually going to scale. It is not going to arrive as a single disruptive technology that replaces everything at once. It is going to arrive as a partnership between three kinds of organizations: a global third party logistics provider that controls the freight network, a specialized autonomous trucking startup that provides the vehicle technology, and a major manufacturer that generates the consistent, high volume freight demand needed to fill the trucks on both directions of the route.

That triangle matters. A startup building self driving technology cannot also build a nationwide logistics network from scratch. A logistics giant cannot build its own autonomous driving stack overnight. And a manufacturer cannot afford to wait for either of them to figure it out alone. When all three come together around a specific corridor, the result is not a science experiment. It is a commercial operation with real revenue on both sides of the trip.

The implications for the freight industry are broad. Start with freight rates. Autonomous trucks can run nearly continuously, limited only by fuel stops and regulatory driving windows for the humans who still handle the tricky portions of the route. That means more capacity on the same lane, which puts downward pressure on rates. Shippers will benefit. Carriers that do not adopt autonomy will find themselves priced out of the most efficient lanes.

Then consider insurance. Autonomous trucking introduces a shift from driver risk to technology risk. Who is liable when a sensor fails or a decision algorithm makes the wrong call on a highway merge? The current insurance model is built around a human driver with a license and a record. A truck with no driver, or a driver who is only present for the first and last mile, does not fit that framework. New insurance products will need to emerge, and the early operators who demonstrate strong safety records will define the underwriting standards for everyone else.

The driver labor question is the most emotionally charged, but it is also the most misunderstood. Autonomous trucks will not eliminate driving jobs overnight. What they will do is change the nature of the work. The long stretches of interstate highway driving that make long haul trucking grueling and lonely are precisely the parts that autonomy handles best. The first and last mile driving, the yard maneuvers, the customer interactions, the problem solving when a dock door is broken or a shipment is short these are the parts that remain human for a long time. The job shifts from highway pilot to logistics specialist. The number of drivers needed per mile of freight goes down, but the skill required for the remaining roles goes up.

Competition with intermodal rail is another angle worth watching. Rail is already the most fuel efficient way to move freight across long distances, but it suffers from speed and flexibility penalties. Autonomous trucks that can run around the clock on dedicated freight lanes narrow that gap. A shipper choosing between rail and truck on a coast to coast lane will look at transit time, reliability, and cost. If autonomous trucks can match rail on cost while beating it on speed and door to door service, the modal shift could be significant.

What needs to happen next before this scales beyond a single corridor? Three things. First, regulation. The current patchwork of state level rules for autonomous trucks is a barrier to coast to coast operation. A truck that is legal in one state may be restricted or prohibited in the next. Federal framework legislation would unlock the full network effect. Second, infrastructure. Autonomous trucks depend on consistent lane markings, working roadside sensors, and reliable communication networks. Rural highways that lack these basics will be the last to see autonomous service, and that creates a two tier freight system. Third, public acceptance. A single high profile accident involving an autonomous truck could set the industry back years. The early operators must be relentless about safety transparency and community communication.

The round trip milestone matters because it proves that autonomous trucking is not a technology in search of a business model. The business model exists. It runs from coast to coast and back again. Now the question is how fast the industry can build the regulatory and infrastructure scaffolding to let it run everywhere else.