The global energy supply chain is facing one of its most severe tests since the modern oil era began. When a major geopolitical confrontation erupted near the most critical maritime chokepoint in the world, the Strait of Hormuz, the immediate shockwaves were felt across every continent. Yet what is unfolding now is a slow motion drama of risk, resilience, and strategic repositioning that every supply chain professional must understand.

The Hidden Fleet and the Great Escape

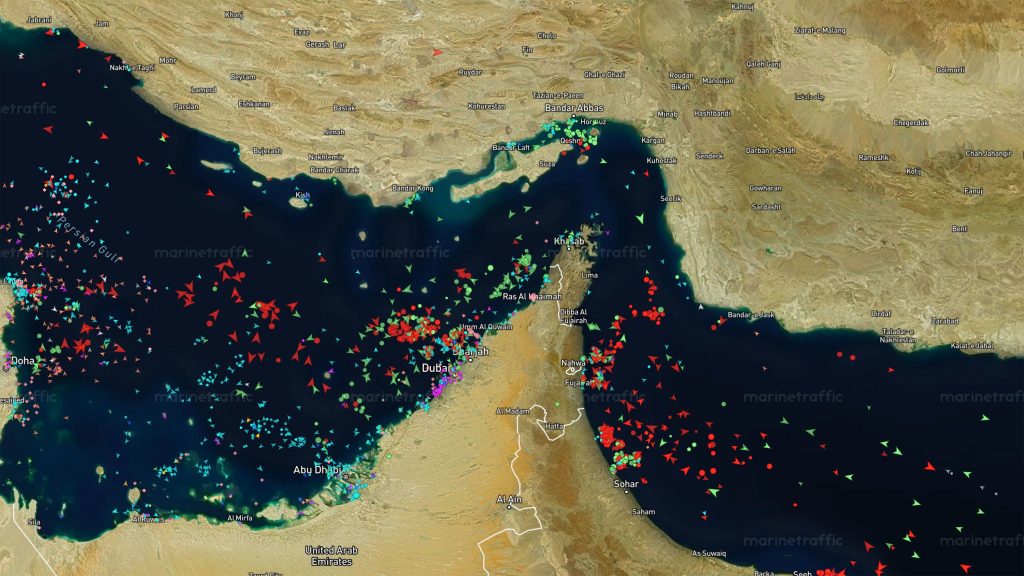

When the conflict erupted and the strait was effectively closed, more than one hundred large oil tankers found themselves trapped inside the Persian Gulf. These were not small vessels. These were very large crude carriers capable of hauling two million barrels of oil each, alongside Suezmaxes and Aframaxes that form the backbone of global crude transportation. For weeks, these ships sat idle, their crews watching as diplomatic channels heated up and military tensions escalated around them.

But a quiet transformation has been underway. Nearly a third of those stranded vessels have now managed to slip out through the chokepoint. They have done so not in a dramatic convoy, but in a slow, stealthy trickle that has largely gone unnoticed outside of specialized shipping circles. Many switched off their Automatic Identification Systems, the maritime equivalent of going dark, to avoid detection. Some navigated alternative routes closer to Oman, bypassing the northern lane controlled by Iranian forces.

The Numbers That Matter

The volumes that have escaped so far amount to roughly 520,000 barrels per day. To put that in perspective, before the crisis the strait carried about one fifth of the entire world’s oil supply. This is not merely an energy story. It is a supply chain story that cascades into manufacturing, logistics, chemical production, and ultimately every sector that depends on affordable energy. When crude supply tightens, shipping costs rise, refinery throughput drops, and the cost of moving goods across the world increases at every node.

What makes this situation particularly dangerous is the global inventory position. Oil stockpiles have been drawing down at a record pace. Every barrel that remains stuck inside the Gulf is a barrel that cannot replenish those strategic reserves. Major oil companies have acknowledged the situation openly, with executives confirming that they have vessels under charter in the zone and are waiting to see whether any diplomatic resolution will hold before sending more ships into the region.

Alternative Routes and the New Supply Chain Calculus

Saudi Arabia and the United Arab Emirates have activated alternative pipeline routes to bypass the strait. These pipelines were designed as contingency infrastructure, investments made during calmer times that are now proving their worth. Yet pipeline capacity is finite, and the volumes they can carry are a fraction of what normally moves through the strait on a daily basis. The gap must be filled by strategic reserves, demand destruction, or higher prices that naturally curb consumption.

The concept of a toll booth has also emerged, with one side of the conflict demanding fees as high as two million dollars per ship for passage along its coastline. Whether these demands have been met remains unclear, but the mere existence of such a proposition signals a fundamental shift in how maritime chokepoints will be governed in the future. Supply chain professionals who once assumed freedom of navigation as a given must now build scenarios where passage through critical straits requires negotiation, payment, or military escort.

What This Means for Your Supply Chain

If your supply chain relies on just in time inventory, energy intensive manufacturing, or chemical feedstocks sourced from global markets, this is not a distant geopolitical story. This is a direct input to your planning assumptions. Inventory buffers that were once considered excessive are now being re evaluated as essential resilience. Dual sourcing of energy intensive inputs is moving from a nice to have to a strategic imperative.

The vessels that have escaped so far are a positive signal. They demonstrate that passage is possible. But they also highlight how fragile the recovery will be. The diplomatic process is ongoing, with preliminary ceasefire extensions being discussed. Yet even if a peace agreement is reached, rebuilding trust in the security of the strait will take months or years. Supply chains do not snap back to normal overnight. They recalibrate slowly, and the new normal will look very different from the old one.

Lessons for the Resilient Enterprise

Three lessons emerge from this crisis. First, chokepoint risk must be modeled explicitly in your supply chain scenario planning. The Strait of Hormuz is not the only critical passage. The Suez Canal, the Panama Canal, the Malacca Strait, and the Turkish Straits all carry similar concentration risk. Second, transparency into your energy supply chain is no longer optional. Knowing where your energy comes from and what route it travels is the foundation of any resilience strategy. Third, the era of assuming stable energy access is over. Every supply chain strategy for the next decade must incorporate energy disruption as a baseline assumption, not an edge case.

The oil that has escaped the Gulf is a reminder that even in the most locked down supply chains, there is always movement. But the pace of that movement, the cost of securing it, and the trust required to maintain it have all changed fundamentally. The question every supply chain leader must now answer is not whether the next chokepoint crisis will come, but whether their network is built to withstand it.