The AI data center gold rush is reshaping more than technology markets. It is now redrawing the map of global energy supply chains. European buyers are paying premiums just to secure gas turbines, a phenomenon that started in the United States and has quickly gone global.

Siemens Energy AG CEO Christian Bruch confirmed that customers in Europe are now willing to pay reservation fees to secure a spot in production queues. The practice first emerged in the U.S. as technology companies rushed to secure generation capacity for energy-hungry data centers. It has since spread to Europe and the Middle East.

Customers seeking to reserve manufacturing slots for about six months typically pay between 10 and 15 percent of a turbine purchase price, according to Karim Amin, the head of Siemens Energy gas services unit. With turbine manufacturers largely booked through the end of the decade, these payments have become the only way for buyers with urgent projects to secure a place in the queue. Siemens Energy conversion rate is above 90 percent, meaning most reservations eventually become firm contracts.

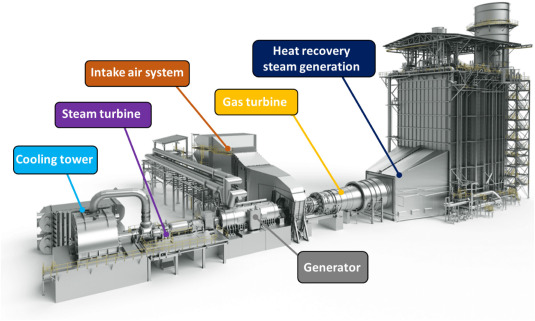

The implications for supply chain professionals are significant. Three companies dominate the global gas turbine market: Siemens Energy, GE Vernova and Mitsubishi Power. All three are running near full capacity. Lead times have stretched from months to years. For manufacturers and data center developers racing to secure power, this creates a new bottleneck that did not exist just three years ago.

What does this mean for companies that depend on stable energy infrastructure? First, the cost of new power generation capacity is rising. Siemens Energy declined to specify exact price increases, but the willingness of buyers to pay reservation fees tells its own story. Second, the queue is getting longer. Projects planned for 2027 or 2028 may not find available manufacturing slots unless reservations are made now. Third, competition for turbines is no longer limited to utilities. Data center operators are now direct competitors for the same equipment.

The squeeze is particularly relevant for countries that need gas-fired plants to back up power grids relying heavily on intermittent renewables. Germany plans to start auctions in September to support construction of 9 gigawatts of new gas-fired plants. Siemens Energy is already in talks with several prospective bidders. The outcome of these auctions will test whether national energy programs can compete with data center demand in a constrained supply market.

Data centers currently account for about 25 percent of Siemens Energy turbine demand, while roughly 60 percent comes from conventional applications such as utilities. The company wants to maintain that balance. It deliberately held back capacity for utilities and national power programs to avoid becoming too dependent on one source of demand. As Amin put it, no business grows all the time. The strategy is to ensure current orders generate service revenues for decades. The company roughly 87 gigawatts of recent orders should generate about 35 billion euros in service business over more than 20 years.

For supply chain leaders, this situation demands attention. Energy infrastructure procurement is no longer a routine utility function. It has become a strategic competitive issue. Companies that depend on new power capacity for data centers, manufacturing expansion or electrification projects need to factor turbine availability and lead times into their planning cycles.

The reservation fee model is a signal that the market has fundamentally changed. When buyers are willing to pay a premium just to get in line, it means demand is structurally exceeding supply. This is not a temporary spike. The buildout of AI infrastructure, electrification and grid modernization will continue for at least the rest of this decade.

The lesson is straightforward. Energy supply chains are now a constraint on AI growth. The companies that recognize this early and adjust their procurement strategies accordingly will have a meaningful advantage over those that treat power availability as someone else problem.